The Pareto Principle, also known as the 80/20 Rule, refers to a statistical regularity observed in a number of areas. According to this rule, 80% of overall value comes from 20% of the most important items. Procurement has embraced this principle to prioritise its purchases using three categories: A, B and C also named Tail spend. However, appearances can be deceptive.

What is the Pareto Principle?

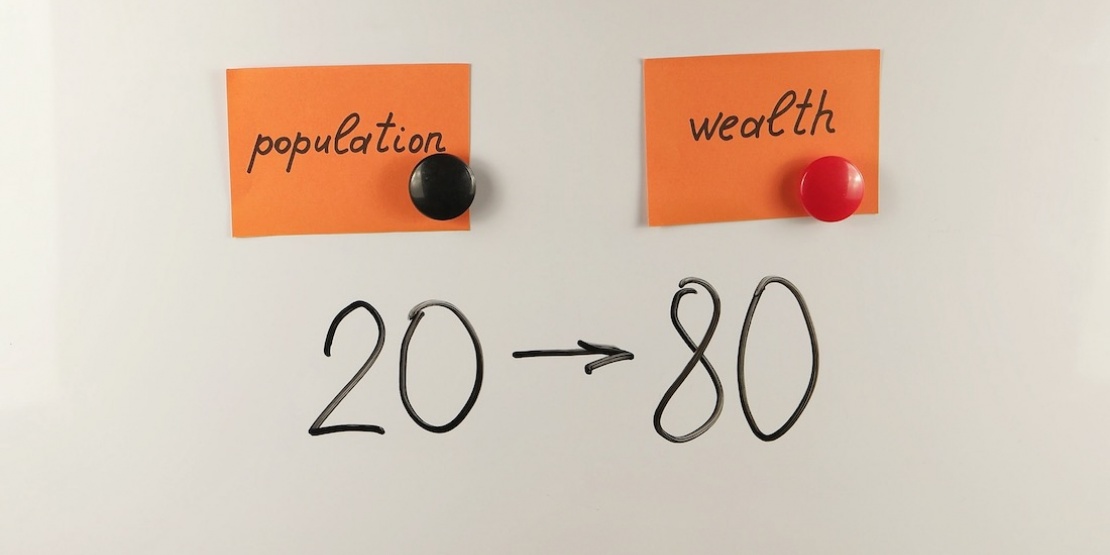

In the 19th century, Italian sociologist and economist Vilfredo Pareto conducted a statistical study on income inequality in Italy. The study found that, on average, 80% of the country's wealth was held by 20% of its population. Intrigued by this observation, he then converted this income-distribution law into a mathematical formula.

A few decades later, Joseph Moses Juran coined the term "Pareto Principle" to mean that about 80% of overall value is produced by 20% of the most important items. This statistical regularity, also known as the 80/20 Rule, has since been observed in many areas.

For example, it is said that:

- 80% of a company's turnover is generated by 20% of its customers

- 80% of income tax comes from 20% of earners

- 80% of storage space is occupied by 20% of products

- 80% of complaints are made by 20% of customers

This rule highlights the importance of optimising resources to achieve the best return. In other words, we need to focus on the 20% to produce 80% of the results. In the world of procurement, this raises the issue of cost optimisation.

Class A, B and Cpurchases, also named Tail spend

Procurement uses a Pareto-inspired classification system known as the "ABC Method" to prioritise its purchases.

There are three distinct categories:

- Class A purchases account for 80% of the total cost of purchases for 20% of suppliers

- Class B purchases account for 15% of the total cost of purchases for 30% of suppliers

- Class C purchases, also named Tail spend account for 5% of the total cost of purchases for 50% of suppliers

In line with the Pareto Principle, procurement departments have focused on controlling purchases with a significant impact on overall value, i.e. Class A or maybe Class B.

The third category, which on the face of it is not as important, has long been neglected by buyers. However, the reality is quite different. Although they represent just 5% of total purchase costs, Tail spend account for the majority of indirect costs (managing suppliers, placing orders, costs of poor quality, unscheduled purchases etc.). Therefore, when viewed through the lens of TCO (Total Cost of Ownership), Tail spend clearly deserve procurement departments' attention.

Optimising Tail spend is now a means of giving a company a competitive advantage, or can even demonstrate a certain level of maturity within their procurement departments.