TCTO, or Total Cost of Temporary Ownership, is an emerging concept in the world of procurement. It enables the calculation of the total cost of an asset for a limited period of use, incorporating both the costs of ownership over a given period and the anticipated resale value. Inspired by the well-known TCO, this approach fits within both an economic and circular logic.

From TCO to TCTO

TCO, Total Cost of Ownership, evaluates all costs associated with purchasing and using a good or service throughout its entire life cycle. This calculation method, well known to buyers, takes into account direct and indirect costs.

TCTO, Total Cost of Temporary Ownership, applies when this good or service is used for a defined period of time. In this case, resale also becomes a key optimisation lever.

This approach makes it possible to determine the net cost of temporary use. The calculation method is refined by taking into account the actual duration of use and resale. Buyers can then compare different scenarios and define the optimal time to dispose of this asset.

How to calculate TCTO?

TCTO features the same components as TCO, whilst adding elements associated with the duration of use and resale.

The basic formula

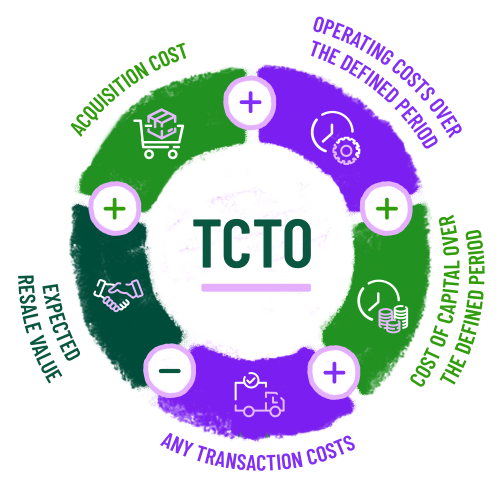

TCTO = Acquisition cost + Operating costs over the defined period + Cost of capital over the defined period + Any transaction costs – Anticipated resale value.

Acquisition costs

First, there is the purchase price or the first rent paid. To this must also be added the associated acquisition costs: taxes, delivery and installation costs, employee training costs...

Operating costs

This includes all routine operating costs during the given period of use. This covers maintenance and repair costs, operating costs such as energy consumed, insurance, consumables, storage costs... Not forgetting downtime costs in the event of breakdown or immobilisation.

Cost of capital

These are the financing costs over the defined period. This includes interest when the purchase is financed by loan or leasing, or the opportunity cost of funds tied up in a cash purchase.

Transaction costs upon resale

The costs associated with early disposal must not be overlooked. This covers the costs of cleaning, repairing or refurbishing the goods before sale, intermediary commissions, logistics costs including transport, dismantling or removal, but also regulatory costs such as secure data erasure for IT equipment.

Anticipated resale price

Lastly, this is an essential component of TCTO: the residual value. This involves estimating the potential resale value of the asset at the end of the period of use. In particular, the depreciation of the asset and the state of the second-hand market must be taken into account. This figure counterbalances all the costs previously mentioned.

When to use TCTO?

The key question is knowing when to favour calculating TCTO over TCO, and vice versa.

As Didier Sallé, the French President of the National Procurement Council points out: "There is no absolute solution for determining TCO in all procurement departments. For truly relevant solutions, it is much better to consider the specifics of each line of business".

TCTO

Procurement departments have every interest in calculating TCTO whenever the use of a good is temporary and its resale value is strategic in the decision-making process. This concerns, for example, warehouse and workshop equipment, vehicle fleets, construction equipment...

Buyers can compare models (long-term purchase, purchase/resale, rental or even leasing), determine the optimal period of use, or calculate the cost of a usage cycle within a circular logic.

Manutan Group, your circular partner

Manutan Group positions the circular economy at the heart of its business model. This is why we offer second-hand products as well as value-added services such as the collection and revaluation of your old equipment and product rental.

TCO

Conversely, procurement departments will use TCO when they need to consider the complete life cycle, with no resale horizon. These are all the goods that the company intends to keep or which have a low resale value: office furniture, software solutions, bespoke equipment...

Through TCO, procurement teams can compare several solutions over their entire life cycle. This method thus serves as a decision-making tool for the long term and as a basis for negotiations with suppliers.

Proof through example

Let's take the example of a company preparing for an increase in activity over the next three years, following the signing of a new contract. It is about to recruit new employees, requiring the installation of around ten additional workstations. Because the volume of activity remains uncertain beyond this period, the company is hesitating between various models: purchase/resale, second-hand purchase and rental, not forgetting leasing for IT equipment.

Desks

For desks, the second-hand and rental markets are competitive. These options reduce the cost of capital and the risk associated with resale.

- With the purchase/resale of new and standard products, we obtain:

€3,200 purchase (around £2,770) + €400 assembly/delivery (around £350) + €684 cost of capital (around £590) – €800 resale (around £690) = €3,484 (around £3,000)

- With second-hand purchase:

€1,800 purchase (around 1,560) + €400 assembly/delivery (around £350) + €386 cost of capital (around £335) = €2,586 (around £2,240)

- With rental:

€2,160 rental (around £1,870) + €400 assembly/delivery (around £350) = €2,560 (around £2,200)

Office chairs

In the case of ergonomic office chairs, these have an interesting residual value. Purchase/resale then appears to be the right option. However, cost differences are more tightly aligned between each option.

- With the purchase/resale of new and standard products, we obtain:

€1,940 purchase (around £1,680) + €200 assembly/delivery (around £170) + €415 cost of capital (around £360) – €1,000 resale (around £865) = €1,555 (around £1,345)

- With second-hand purchase:

€1,240 purchase (around £1,075) + €200 assembly/delivery (around £170) + €265 cost of capital (around £230) = €1,705 (around £1,475)

- With rental:

€1,440 rental (around £1,245) + €200 assembly/delivery (around £170) = €1,640 (around £1,420)

Computers and phones

For IT equipment, usage-based models (rental or leasing) reduce exposure to obsolescence, maintenance and financial immobilisation. This makes them efficient options over a defined period.

- With the purchase/resale of new and standard products, we obtain:

€8,000 purchase (around £6,900) + €500 installation/delivery (around £430) + €1,710 cost of capital (around £1,480) + €600 maintenance (around £520) – €3,200 resale (around £2,770) = €7,610 (around £6,590)

- With second-hand purchase:

€4,800 purchase (around £4,150) + €500 installation/delivery (around £430) + €1,026 cost of capital (around £890) + €900 maintenance (around £780) = €7,226 (around £6,250)

- With rental:

€5,400 rental (around £4,670) + €500 installation/delivery (around £430) = €5,900 (around £5,100)

- With leasing:

€4,320 rental (£3,740) + €500 installation/delivery (around £430) = €4,820 (around £4,170)

This example clearly shows how TCTO reveals hidden costs and risks but also the benefits associated with each model. This enables buyers to make informed decisions.

The full benefit of TCTO

First, TCTO contributes to expenditure management. Buyers can use it to reduce the net cost of ownership, optimise the retention period, limit the immobilisation of capital... This provides key information to inform decision-making and encourage the adoption of new practices. For example, collection and revaluation scenarios can be integrated into tenders.

Beyond the financial aspect, TCTO also fits within a circular economy logic, as the company optimises the use of its resources and limits waste.

This approach particularly encourages:

- Considering alternatives to purchase: rental, leasing, product as a service...

- Preparing for the second life of purchased products by taking into account their resale value

- Favouring the purchase of durable, quality goods that will have a future in the second-hand market.

Ultimately, TCO remains the reference for comparing suppliers, anticipating costs and guiding strategic decisions beyond the simple purchase price. TCTO, on the other hand, constitutes a variant adapted to more specific cases. The idea is, therefore, not to oppose these two concepts, but rather to opt for the most relevant calculation method according to the context.